Beyond U.S. Markets: Why European Covered Calls Deliver Superior Income

- Jan 6

- 5 min read

Many investors have been drawn to the high-yielding, lower risk profile of U.S.-focused covered call strategies. The surge in popularity has attracted over $100 billion in inflows over the last three years (2022-2025). This trend accelerated into record inflows in 2025, driven by investors seeking higher yields and a buffer against market volatility.

Understanding Covered Call Strategies

How It Works

In a covered call strategy, the options technique used most by institutional investors involves selling call options against owning the underlying security. Here is the process:

Buy the Stock: Acquire shares of a company you want to hold.

Sell a Call Option: Grant another investor the right to purchase your shares at a predetermined price (the strike price) by a specific date.

Collect a Premium: Receive immediate income for selling this option.

Three possible outcomes exist:

Stock stays below strike price: The option expires worthless, and you keep both the stock and the premium as profit.

Stock rises above strike price: The option is exercised, meaning you must sell your shares at the strike price. This locks in a profit (stock gain plus premium) but means you miss out on further gains above that price.

If the stock drops: The upfront premium you collected acts as a partial offset against the decline, providing limited downside protection. However, you remain exposed to the full downside risk of stock ownership minus the premium received.

Why The Covered Call Strategy Is Popular

Income Generation: Creates a regular income stream from stocks you already own. By systematically selling call options, investors can generate monthly or quarterly cash flow regardless of whether the stock price appreciates.

Income in Flat Markets: Profitable when stocks trade flat or rise modestly. Traditional buy-and-hold strategies produce no returns in stagnant markets, but covered calls continue generating premium income.

Defined Exit Strategy: Allows you to establish a predetermined selling price for your holdings. This feature provides discipline in volatile markets by removing emotional decision-making from the selling process. When you write a covered call at a specific strike price, you're essentially committing to sell at that level if the stock reaches it. This acts as an automated profit-taking mechanism—you capture gains up to the strike price plus the premium received, creating a clear exit plan. The strike price selection becomes a deliberate choice about acceptable returns rather than a reactive decision made during market turbulence.

The Volatility Advantage

This covered call strategy can be particularly powerful during times of high volatility, since the call premium is closely related to volatility. As volatility increases, so does the premium. Because of this relationship, the strategy can better protect itself against volatile downturns with these higher premiums. It also can recover strongly from downturns since volatility typically decreases slowly, resulting in higher premium income as the elevated premiums usually last for months after the initial downturn. Reinvesting those higher premiums during that downturn allows the strategy to not only protect against downside risk but also increase potential upside, as buying new shares at lower prices becomes possible with the additional cash from premiums collected.

Option premiums also vary across different regions, industries, and growth factors. High-risk or growth industries, like semiconductors or certain fast-moving healthcare stocks, have higher premiums than defensive sectors, while European securities often have higher option premiums than their U.S. counterparts.

European Markets Offer Higher Returns

Higher Premiums from Volatility

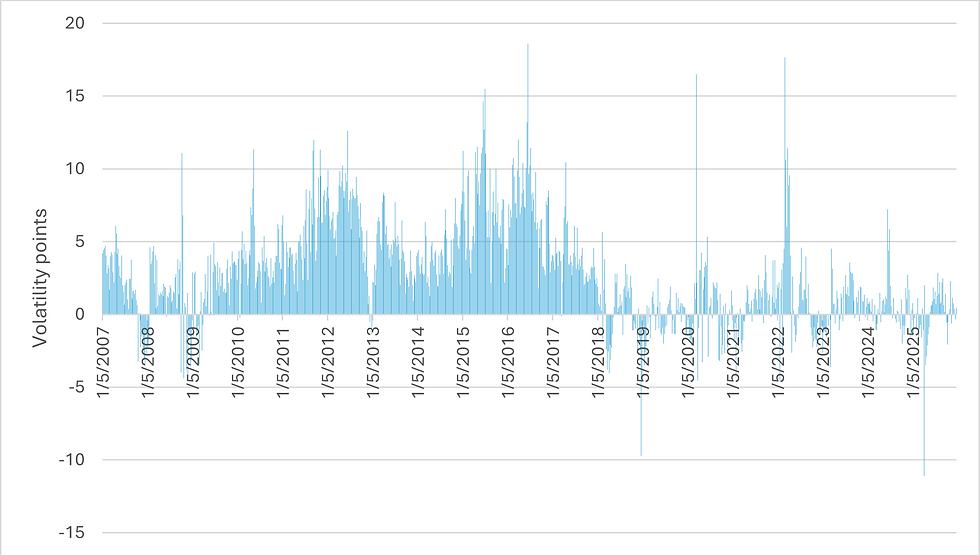

Based on historical data, option premiums on the STOXX 50 are higher than on the S&P 500. This is mainly due to the STOXX 50 trading at a higher implied volatility level than the S&P 500. Figure 1 below shows how the STOXX 50's volatility index, VSTOXX, is often higher than the volatility index of the S&P 500, VIX, indicating that the STOXX 50 is more volatile than the S&P 500.

The STOXX 50's 4.5-Point Average Higher Volatility than the S&P 500

VSTOXX minus VIX

Figure 1: The STOXX 50 volatility index VSTOXX minus the S&P 500 volatility index VIX since January 5, 2007. A positive value means the VSTOXX is higher than the VIX, while a negative means the VIX is higher (Source: Bloomberg)

As illustrated above, the STOXX 50 shows a 4.5-point average higher volatility than the S&P 500. This additional volatility also comes with higher expected dividends and more attractive forward P/E levels in the STOXX 50, as well as regional differences in skew.

Additional Benefits: Dividends and Valuations

Premiums are not only based on the implied volatility of an industry or region but also other factors relating to individual equities. Two additional factors make European markets particularly attractive for covered call strategies: dividend yields and valuations.

Superior Dividend Yields

European companies have historically maintained higher dividend payout ratios than their U.S. counterparts. The STOXX 600's dividend yield is over 150% higher than the S&P 500. This matters for covered call investors because dividends represent an additional income stream on top of option premiums. When you own European stocks as part of your covered call strategy, you're collecting both the option premium and notably higher dividend payments, compounding your total return. This dual income approach can significantly enhance overall portfolio yields, particularly in flat or moderately rising markets where covered call strategies tend to perform best.

More Attractive Valuations

European large-cap stocks currently trade at more attractive forward price-to-earnings (P/E) ratios compared to U.S. equities. Lower valuations provide two advantages for covered call investors. First, they offer a better entry point with more reasonable purchase prices, reducing the capital required to establish positions. Second, lower valuations typically correlate with less downside risk during market corrections, as highly valued stocks tend to experience sharper declines when sentiment shifts. This valuation cushion complements the downside protection provided by option premiums, creating a more defensive overall position.

Combined with higher implied volatility driving larger option premiums, these fundamental advantages, superior dividends and attractive valuations, create a compelling case for European-focused covered call strategies. Investors benefit from multiple income streams and better risk-adjusted returns compared to similar U.S.-based approaches.

Conclusion

The STOXX 50 consistently exhibits higher volatility than U.S. markets. This elevated volatility environment means that focusing a covered call strategy on Europe is expected to result in higher premiums and higher yields, even on stocks that move similarly to their U.S. counterparts. This could give investors a more predictable high cash return and allow for greater loss protection during times of market volatility.

For More Information

Institutional investors interested in learning more about the Lucerne European Income Select Fund, see our introduction video or contact us:

Thijs Hovers

Lucerne Capital Management, L.P.

Email: th@lucernecap.com

Phone: +1 (203) 983-4400

General Inquiries: irelations@lucernecap.com

73 Arch Street

Greenwich, Connecticut 06830